[Chemical Materials] Thermal-conductive adhesive is expected to take off aggin with the help of new energy vehicles.

[Chemical Materials] Thermal-conductive adhesive is expected to take off aggin with the help of new energy vehicles.

With the accelerating implementation of the fast charging of new energy vehicles and the improving energy density of batteries, higher requirements are put forward for thermal management. Thermal conductive and heat insulation materials in new energy vehicles usher in demand growth. Benefiting from the release of the CTP battery process, thermal conductive/structural adhesives have a vast market. It is estimated that the value of thermal/structural adhesives in CTP-equipped vehicles will rise from RMB 200-300/vehicle in the traditional industry to RMB 800-1000/vehicle. Some institutions predict that the national/global automotive adhesives and parts market will reach about RMB 15.4/34.2 billion by 2025.

Key Point: The components of traditional automotive adhesive are mainly epoxy resin and acrylic acid, but their low elasticity cannot meet the respiration demand of power batteries. Polyurethane and silicone systems with high elasticity and adhesive strength are expected to dominate the market and benefit relevant chemical enterprises.

[Photovoltaic] The demand for photovoltaic drives trichlorosilane to take off.

The main application of trichlorosilane (SiHCl3) is polysilicon used in solar cells, and it’s a core raw material for polysilicon production. Influenced by the rapid growth of photovoltaic demand, the price of PV-grade SiHCl3 has risen from RMB 6,000/ton to RMB 15,000-17,000/ton since this year. And domestic polysilicon enterprises are expanding rapidly in the context of green energy transformation. The demand for PV-grade SiHCl3 is estimated to be 216,000 tons and 238,000 tons in the coming two years. The shortfall of SiHCl3 may be intensified.

Key Point:The “50,000 tons/year SiHCl3 project” of the industry leader Sunfar Silicon is expected to be put into production in the third quarter of this year, and the company also plans a “72,200 tons/year SiHCl3 expansion project”. In addition, many listed companies in the industry have PV-grade SiHCl3 expansion plans.

[Lithium Battery] The cathode material explores a new direction of development, and lithium manganese ferro phosphate ushers in development opportunities.

Lithium manganese ferro phosphate has high voltage, high energy density, and better low-temperature performance than lithium ferro phosphate. Nanominiaturization, coating, doping, and microscopic shape control measures gradually improve LMFP conductivity, cycle times, and other shortcomings by one or synthesis. Meanwhile, while ensuring the electrochemical performance of the material, mixing LMFP with ternary materials can greatly reduce the cost. Leading domestic battery and cathode companies are accelerating their patent reserves and have started mass production planning. Overall, the industrialization of LMFP is speeding up.

Key Point:As the energy density of lithium ferro phosphate has almost reached the upper limit, lithium manganese ferro phosphate may become the new development direction. As the upgraded product of lithium ferro phosphate, LMFP has a broad future market. If LMFP starts mass production and application, it may significantly boost the demand for battery-grade manganese.

[Packaging] Tesa, the world’s leading tape manufacturer, launches rPET packaging tape.

Tesa, the world’s leading provider of adhesive tape solutions, has expanded its range of sustainable packaging tapes with the launch of new rPET packaging tapes. To reduce the consumption of virgin plastics, used PET products, including bottles, are recycled and used as raw material for the tapes, with 70% of PET coming from post-consumer recycling (PCR).

Key Point:rPET packaging tape is suitable for light to medium weight packaging up to 30kg, with a robust, abrasion-resistant backing and a reliable and consistent pressure-sensitive acrylic adhesive. Its high tensile strength makes it comparable to PVC or biaxially oriented polypropylene (BOPP) tapes.

[Semiconductor] Industry giants compete for Chiplet. Advanced packaging technology is gaining momentum.

Chiplet interconnects small modular chips to achieve heterogeneous integrated systems, enabling advanced processes while reducing manufacturing costs. It is a new technology in the post-Moore era, widely used in data centers and the consumer electronics market, the market size of which is expected to reach $5.8 billion in 2024. AMD, Intel, TSMC, Nvidia, and other giants have entered the field. JCET and TONGFU also have a layout.

Key Point:The storage and computing convergence framework will be needed by the market. Chiplet-led advanced packaging technology will occupy a key part in this field.

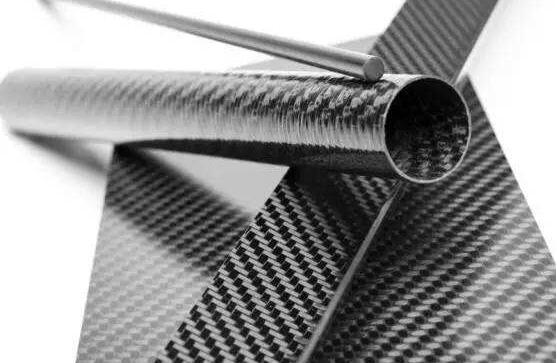

[Carbon Fiber] China’s first set of large-tow carbon fiber production lines has been delivered.

Shanghai Petrochemical of Sinopec has recently delivered the first large-tow carbon fiber production line, and the project equipment has all been installed. Shanghai Petrochemical is the first domestic and the world’s fourth enterprise to master large-tow carbon fiber production technology. With the same production conditions, large-tow carbon fiber can significantly improve the capacity and quality performance of the single fiber and reduce costs, thus breaking the application limitations of carbon fiber due to its high price.

Key Point:Carbon fiber technology has strict technical barriers. Sinopec’s carbon fiber technology has its own intellectual property rights, with 274 relevant patents and 165 authorizations, ranking first in China and third in the world.

Post time: Aug-20-2022